Do you ever feel like money has its hold on you, sometimes even leaving you stressed out and lacking the peace you desire?

From lots of experience, we’ve seen people struggle in this fashion, even at higher levels of net worth and affluence. It’s almost like there is never enough, or it’s a relative concept or something.

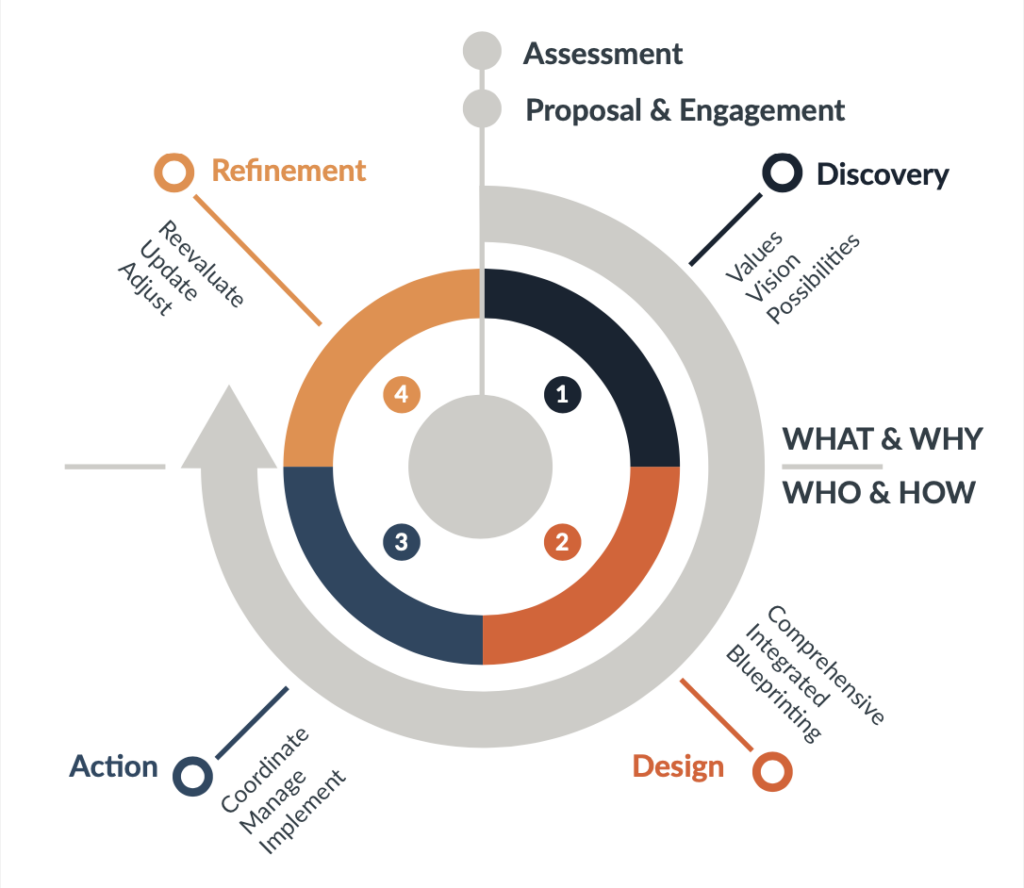

Most people, however, would readily agree that they’d prefer having a clear sense that they are all set financially. They would also like to be able to tie their wealth to what they really care about. That’s the purpose of our LifePrint™ Planning Process.

Using our flagship LifePrint™ Planning Process, as well as our numerous tactical processes, we help individuals, families and business owners realize a secure life for themselves, plan a thoughtful legacy, and oftentimes create a lasting significance through philanthropic giving.

Together, these approaches provide an integrated and comprehensive suite of financial, estate, and tax planning, as well as investment advisory and fiduciary life insurance services, designed to help people maximize the impact of their financial potential during life and through an ongoing legacy they can leave behind.

We’ve observed that most people who have been able to create a deeper understanding and connection between their money and the things they care about most (their “purpose”), are able to realize an enhanced sense of peacefulness, freedom, and impact.

How do you begin to move in this direction? The answer is actually similar to many other areas of our lives. If we need to accomplish something outside of our realm of expertise, we find a capable, skilled, and experienced resource and delegate to some extent, right?

That’s our purpose at Trove. We’re a team of experienced advisors who can help you have the right conversations and begin this process of self-discovery and strategic planning. Your LifePrint™ has so much more potential. Go after it!

You may know some people who seem to turn everything they touch into gold, while others may spend a lifetime working diligently with little to show for their efforts. Is it fate, or is something going on behind the green curtain?

We believe it’s the latter. Because in the world of wealth management, it may not be as much a matter of what you have, but what you do with what you have.

Our years of experience helping families and businesses successfully grow and protect their wealth have produced a time-tested formula composed of the following elements (the boxes below are live, so you can see the various important variables in the formula).

WM (WEALTH MANAGEMENT)

CP (Comprehensive Planning)

IC (Investment Consulting)

RM (Relationship Management)

CP (COMPREHENSIVE PLANNING)

WE (Wealth Enhancement: Tax Mitigation and Cash-Flow Planning)

WT (Wealth Transfer: Transferring Wealth Effectively; may not be within a family)

WP (Wealth Protection: Risk Mitigation, Legal Structures and Transferring Risk to Insurance Company)

CG (Charitable Giving: Maximizing Charitable Impact)

Management of all investment elements to maximize the probability of clients achieving all that is important to them.

RM (RELATIONSHIP MANAGEMENT)

CRM (Client Relationship Management)

PNRM (Professional Network Relationship Management)

We believe that an optimal investment strategy is imperative for any financial plan. History has proven that interest-generating investments such as cash and bonds have relative stability of principal. However, they provide little opportunity for real long-term growth due to their susceptibility to interest rates and inflation. On the other hand, equity investments have clearly enjoyed significantly higher long-term risk-adjusted returns historically, but are vulnerable to more severe volatility risk in the markets. To balance the need for safety and performance, we use several investment platforms to bridge the gap between traditional and alternative investment strategies. They allow us to identify and design the best investment strategy for your situation, and answer questions such as:

After establishing separate accounts and aggregating these into ‘buckets’ tied specifically to one or more of your various financial objectives, we then consider these variables for each bucket, which include among other things your risk tolerance, time horizon, tax sensitivity, income requirements, and more. In this way, we can more strategically optimize your asset management and position you for greater success relative to your various financial objectives. Our most important goal, when it comes to our investment advisory services, is not gathering and retaining your assets, as it is for many in our industry. Instead, our most important focus is to create a next-level investment plan that fuels your confidence to let more of your money go, as you live more generously and share with others the experience of a truly wealthy life!

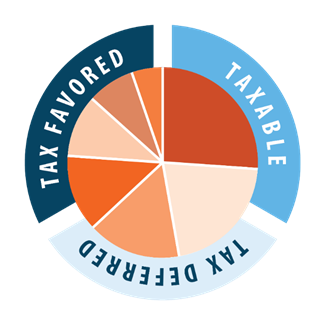

When planning for retirement, diversification typically references an investment allocation that incorporates various asset classes. However, a truly diversified investment strategy should go one level deeper, taking into consideration the tax treatment of one’s retirement savings. We call this Diversification 2.0.

Traditionally, individuals accrue the bulk of their retirement savings in tax-deferred, qualified accounts such as 401Ks, 403Bs, and IRAs, but these one-dimensional savings strategies limit one’s flexibility to mitigate tax liability during retirement.

Diversification 2.0 involves accumulating investment savings in tax deferred, tax favored, and taxable accounts during our working years. Implementing a customized Diversification 2.0 strategy gives investors the ability to better control this issue by making intentional withdrawals from various retirement accounts with different tax characteristics.

One benefit of this strategy may include the reduction of necessary gross portfolio withdrawals to meet a specified income objective, preserving the longevity of a retiree’s nest egg.

See the strategies and principles that we follow at Trove in effect in these real-world applications, and discover the lasting impact they make on both families and businesses.

72 Taunton Street

Plainville, MA 02762

P: 781.489.9800

info@trovepw.com

Securities offered through Valmark Securities, Inc., Member FINRA/SIPC. Advisory services offered through Valmark Advisers, Inc., an SEC Registered Investment Advisor. 130 Springside Drive, Suite 300, Akron, OH 44333-2431 · (800) 765-5201. Trove Private Wealth™ is a separate entity from Valmark Securities, Inc. and Valmark Advisers, Inc.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, and CFP® (with plaque design) in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

C12 equips Christian CEOs and owners to build great businesses for a greater purpose.